A new report released by the World Economic Forum (WEF) and the Cambridge Centre for Alternative Finance (CCAF) shows that nearly two-thirds (64%) of financial services leaders expect to be mass adopters of AI in the next two years, compared to just 16% today. These firms plan to expand AI use beyond cost reduction, and use it for revenue generation, process automation, risk management, customer service and client acquisition. However, the study also reveals executive fears surrounding AI bias and market-wide risks. In fact, more than half of the executives interviewed for the study expect mass AI adoption to ‘worsen bias and discrimination’ within the sector.

The report Transforming Paradigms: Global AI in Financial Services Survey, supported by EY and Invesco, explores the impact AI will have on the industry thanks to interviews with over 150 senior financial services executives in both fintech and incumbent financial institutions.

MITIGATING RISKS

Mass AI adoption is expected to exacerbate certain market-wide risks and biases, and at least one in five firms do not believe they are well placed to mitigate them, according to the report. Finance executives are particularly wary of the potential for AI to “entrench biases in decision-making, or to expose them, through shared resources, to mass data and privacy breaches”, the report notes. However, 70% of respondents also believe they are at least somewhat prepared to mitigate AI bias risks. Generally, those firms using Risk and Compliance teams in AI implementation are more confident about their chances.

The survey also identified other market-wide risks, such as the potential for AI in credit analytics to exacerbate bias in lending decisions. It shows that almost half of all finance executives believe that bias in credit analytics does currently exist and that AI will exacerbate that bias, with a further 15% stating that AI will, in fact, introduce bias.

WAR FOR AI TALENT

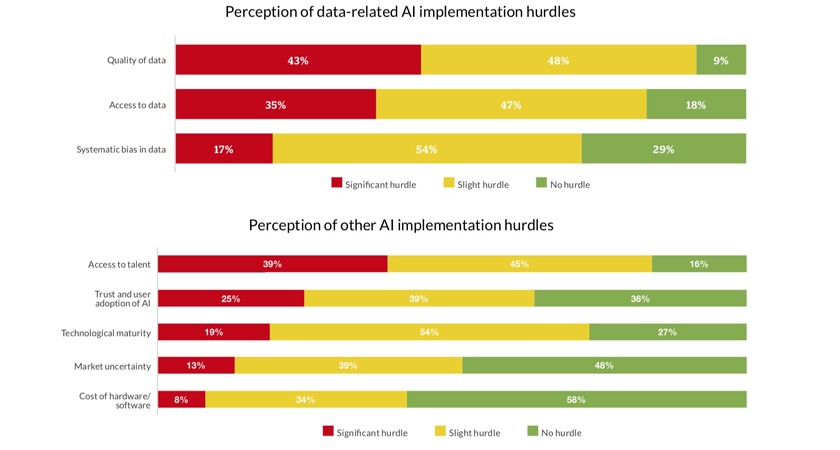

Sourcing suitable talent in AI is another significant hurdle for the industry, with 84% finance executives indicating it to be an obstacle to AI implementation. This reflects findings from a 2018 report by Baker McKenzie, which stated that 38% of respondents to their study found that the shortage of specialist skills concerning AI technology was the most significant obstacle to implementation.

With increasing AI adoption, the competition for AI experts is also beginning to hot up and involving more sectors and geographies. Executives expect the war for talent for AI experts to intensify even further. In fact, nearly half of the executives surveyed regard ‘big tech’ leveraging AI capability to enter the financial services, as a major competitive threat.

PROFOUND SHIFTS

The survey also highlights the profound shift that AI is bringing to financial services as the pace of AI in the industry accelerates. As companies begin to leverage AI to increase profitability and achieve economies of scale, more changes can be expected within the industry and for consumers. The findings also conclude that there will be a significant gap between firms that quickly implement AI and firms that lag behind.

Other key findings include:

- AI is expected to turn into an essential business driver across the financial services industry in the short run, with 77% of all respondents anticipating AI to possess high or very high overall importance to their businesses within two years. While AI is currently perceived to have reached a higher strategic relevance to FinTechs, incumbents are aspiring to catch up within two years.

- The rising importance of AI is accompanied by the increasingly broad adoption of AI across key business functions. Approximately 64% of surveyed respondents anticipate employing AI in all of the following categories: generating new revenue potential through new products and processes, process automation, risk management, customer service and client acquisition – within the next two years. Only 16% of respondents currently employ AI in all of these areas.

BUSINESS TRANSFORMATION

Commenting on the survey findings, Nigel Duffy, EY Global Artificial Intelligence Leader, states: “AI is transforming the financial services industry and we can expect widespread adoption to continue. As the technologies start to disrupt business models and transform business functions, it’s increasingly important for organisations to focus on the long-term implications of AI adoption: trust in AI, workforce transformation, and how customer and stakeholder value can be radically reimagined.”

“The report highlights the amazing opportunity ahead of us in financial services for using artificial intelligence and machine learning to the benefits of our customers and our organisations,” adds Donie Lochan, Chief Technology Officer, Invesco. “Technological advances such as leveraging intelligence to define investments for customers tied to their personalised goals, improving customer experience through the use of intelligent bots, additional alpha generation via insights from alternative datasets, and operational efficiencies through machine learning automation, will soon become the norm for our industry.”

Click here to access the full report.

Sign up for our newsletter